I am often asked why I did not build on the traditional training models?

Let me state that I have not thrown away traditional accounting concepts!

They do work and have their place. My work is based around them.

What I have changed is the perspective that we are looking at them from.

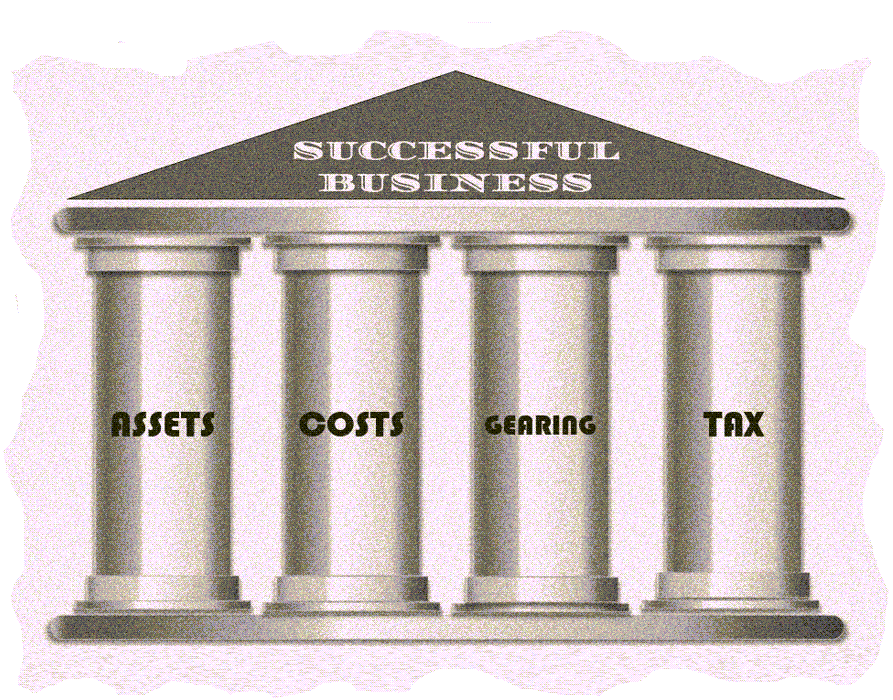

Accounting and finance training relied heavily on this four pillar approach when training candidates in finance.

It was assumed that if people understood these basic elements then they would automatically make informed decisions at work.

A lot of emphasis was placed on the double entry bookkeeping system and how to compile the statutory reports from these records.

The annual Financial Statements have been used for years as the indicator for financial health and we have come to rely on them.

However, they do not address the flaws that exist in the accounting language and too often we ignore these flaws when we train people in finance.

Here is an AI model that was built on the Cash Conversion Cycle which I have compared to my Logic-Model Version of the same process.

In a traditional method the steps in the process are depicted separately and the accounting entries may even be attached to the steps to indicate examples of how the records are compiled. (Often even the AI generated entries contain errors though and in this case I have left them here. See if you can spot them.)

Other problems are that the models are not linked to the next model or other aspects of the business:

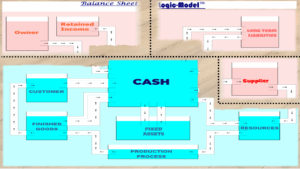

In the Logic-Model™ methodology the models show the steps in the same cycle, however mind maps are being built for later use and applications.

The inter-relationship between the models can be clearly seen for example, the Balance Sheet Logic-Model uses the working capital model as its core building block.

The advantages of this approach include the fact that when doing analysis of financial statements, I use this same model to visually show what is being calculated and how the steps learnt here effect a business’ results for the analysis scenario.

You visually can see the links between the SOCI report and the SOFP report, the accounting going concern principle and the rules of survival all within this one model, which we cannot see in the previous model.