But let us consider these business entities that did traditional accounting and auditing…

Many businesses get themselves into financial difficulties through their leaders making poor business decisions.

What appears to have been a sound strategy at the time, unravels to become a mine field of pitfalls, that has a negative impact on the future financial viability and stainability of the business.

In many of these cases the financial statements were available to the decision makers. They even at times personally may have been involved in compiling some of the reports, yet the business still faced closure as a result of the decisions these leaders had made.

Decisions that looked right within the financial statements!

This phenomena is not only prone to happen to new or young businesses, where it could be argued that the strategy was still developing.

I have come across many entities that have been around for years, that suddenly find themselves facing tough times. This can be due to circumstances outside of the organization or decisions made from within that leadership structure.

What to do in these situations to rectify this, is what is important and these models will help to illustrate the solutions which need to be implemented.

An obvious question posed by many –

“Surely this is only a problem in the start up phases of a business and when the business gets past a certain point, things will pan out naturally and the danger will dissipate?”

Alas, I found that quite the contrary to be true, as these examples above illustrated and I can vouch that I was personally privileged to witness each one first hand.

I either worked for the company involved or I helped them later on get out of the dilemna that they had created. This I achieved , by advising what possible courses of action to take to get out of the hole that they were in. Where did I get the knowledge form?

Well I relied heavily on the insights I had gained from my own models that I had created.

These do not form part of any scientific study or analysis, but rather are what I witnessed first-hand.

Some of the leaders involved in them are still feeling the effects of their poor decision making today.

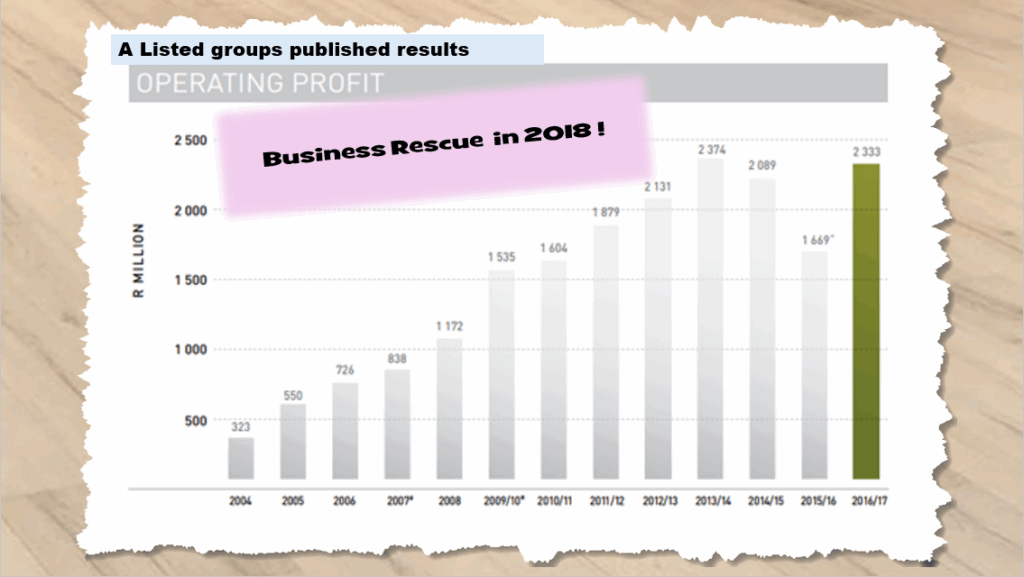

Some people have wondered if these companies were audited properly?

Many students have asked me this question as well.

“Surely the auditors would have seen the problems before any one else did!

One would have thought that this would have been the case. However, in the auditors defence ín each case, they did not really do anything wrong.

Some of these models are designed from a simple business model to allow candidates to better understand business finance.

In that way they are able to identify the financial elements within a business.

They are then able to follow how these elements are shown in the financial records and reports.

More importantly they will visualize what happens to the elements when business decisions are made.

With this insight a business leader is empowered to make more informed decisions and thereby achieve more success.

Participants in the courses are then taken through a process to deconstruct the models again.

By breaking up the reports we are able to illustrate a different perspective of an event.

With these insights many standard conventions and accounting formulae were challenged. Paradigms were reset and a deeper business insight was gained.

I personally found that even though I had formally studied in the finance field, I obtained far more insightful understanding of business finance by developing these models.

With that knowledge I was able to highlight to some of my peers, exactly where our decisions we had made were poor and how we could avoid making such bad decisions again.

When I applied the lessons shown, to given difficulties we were facing as a business entity I was able to help turn the strategic direction of the business around onto a more fruitful path.

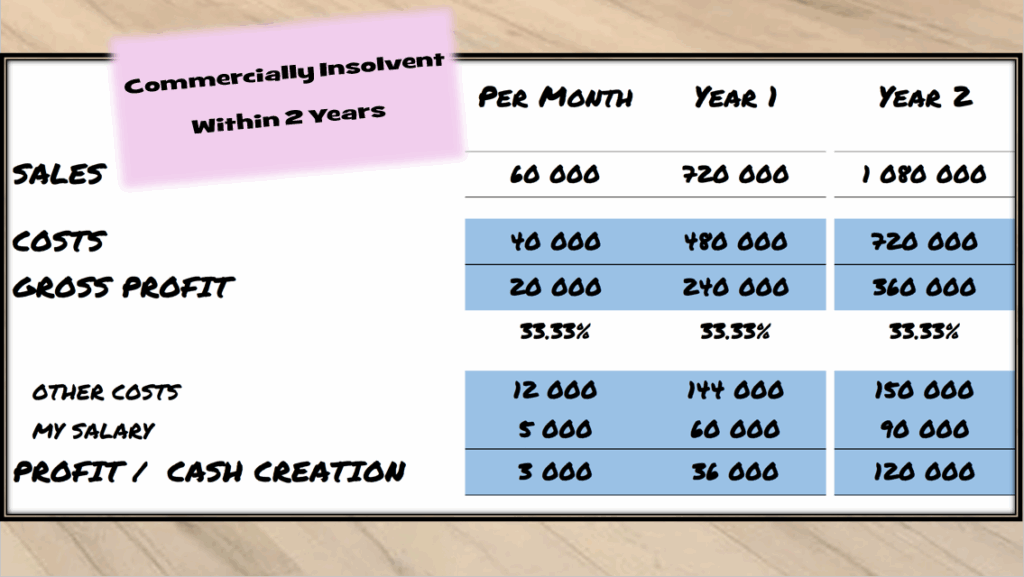

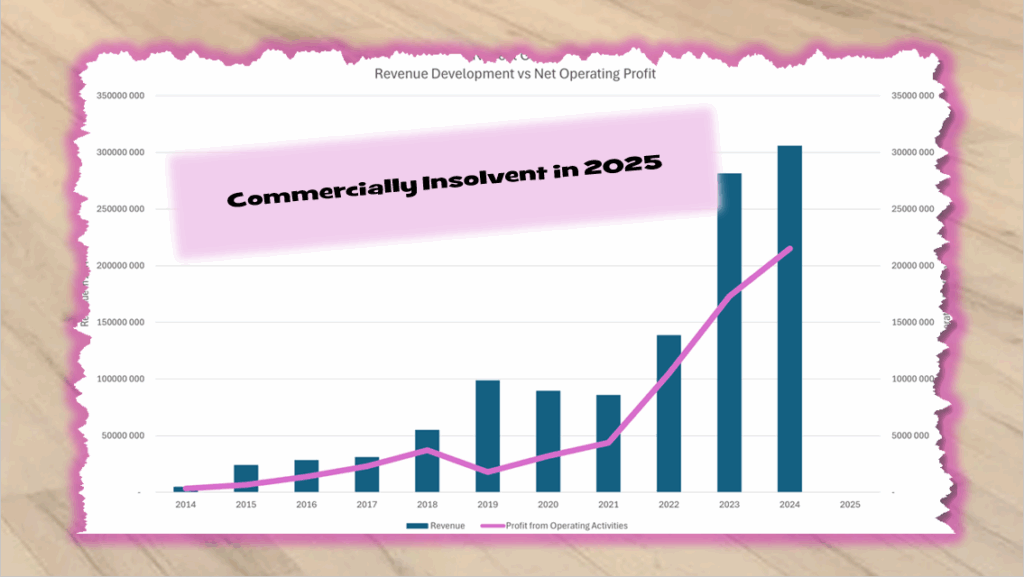

In one such case the team and I were able to triple the size of the business, successfully. Growth is always seen as positive but we ofetn ignore the remaifications it brings.

Not only did we succeed in that goal but we were able to improve our profits by more than 800%. All of this within a period of less than two years !

Then where is the real cause of the problem?

The problems I believe were multifold and having audited financials does not prevent the dangers from affecting the business.

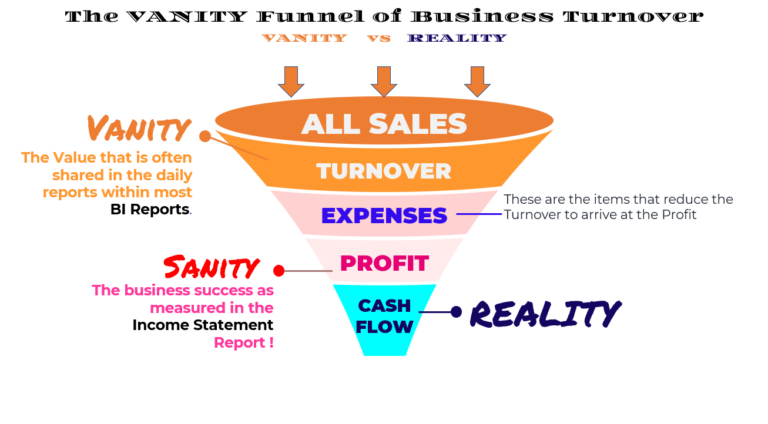

Firstly, there is the problem of our enfatuation with the BRHC principle.

Secondly, there is the problem of the limitations within the accounting language itself.

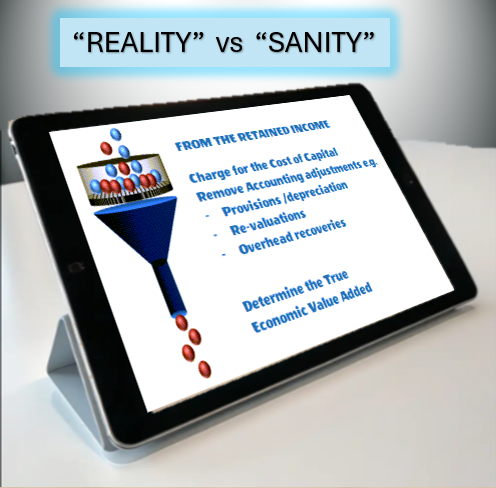

I was lucky enough to work for a large multi-national group, that at the time adopted some of Joel Stern’s philosophies on Econimc Vale Add.

This I later combined with the theories on Throughput accounting that I had been exposed to in another large multi-national I worked for.

This in turn gave rise to me designing another model.

The aim is not to make anyone an expert on

but rather the goal is to use these models to illustrate concepts so that you can avoid making the same or similar mistakes.